Blog

Home / Blog

BancCard Review

- 15th Oct, 2025

- | By Linda Mae

- | Reviews

BancCard is a US based merchant services provider that has been in the payments industry for many years. Known for its community focused model, the company partners with regional banks and local financial institutions to provide payment processing to small and medium sized businesses. This is different from many large fintech companies that focus on scale, automation and online first services. Instead BancCard focuses on relationships, personal service and support through banking partners that merchants already trust. Lets read more about BancCard Review.

In the competitive payments space BancCard is often considered a “middle ground” solution. It may not always have the latest technology or broad international reach but it provides stability and personalized support to local merchants who want reliable processing backed by a familiar banking connection. BancCard’s longevity in the industry is a testament to its ability to adapt to changing technologies while staying true to its partnership model.

For businesses looking at payment processors BancCard is a more traditional approach to merchant services. While newer companies tout app based onboarding and slick interfaces BancCard touts community trust and responsive service. This has its advantages and disadvantages depending on the size of the business, industry and technology requirements.

Table of Contents

ToggleMerchant Onboarding and Application Process | BancCard Review

One of the first steps for any merchant considering BancCard is the onboarding process. Unlike some fintech competitors who offer instant online sign ups, BancCard’s application is typically managed through one of its partner banks or sales reps. Merchants will need to provide standard documentation such as business licenses, bank account information and previous processing statements if available. This process may feel more formal and traditional compared to app based competitors but it ensures a thorough review and reduces approval risk.

Approval times vary but many merchants report accounts are set up within a few business days if documentation is complete. High risk businesses such as those in industries prone to chargebacks may face additional scrutiny or may not be approved at all. It tends to focus on mainstream, low to medium risk industries which aligns with its strong partnerships with regulated banking institutions.

The onboarding process also includes discussions about equipment needs, pricing structure and support requirements. While this may feel slower compared to instant online processors, the hands on approach ensures merchants are matched with the right solutions from the start. For small businesses this can be beneficial especially if they are new to payment processing. But for more tech savvy or fast growing businesses this may feel less agile than what they expect from modern fintech solutions.

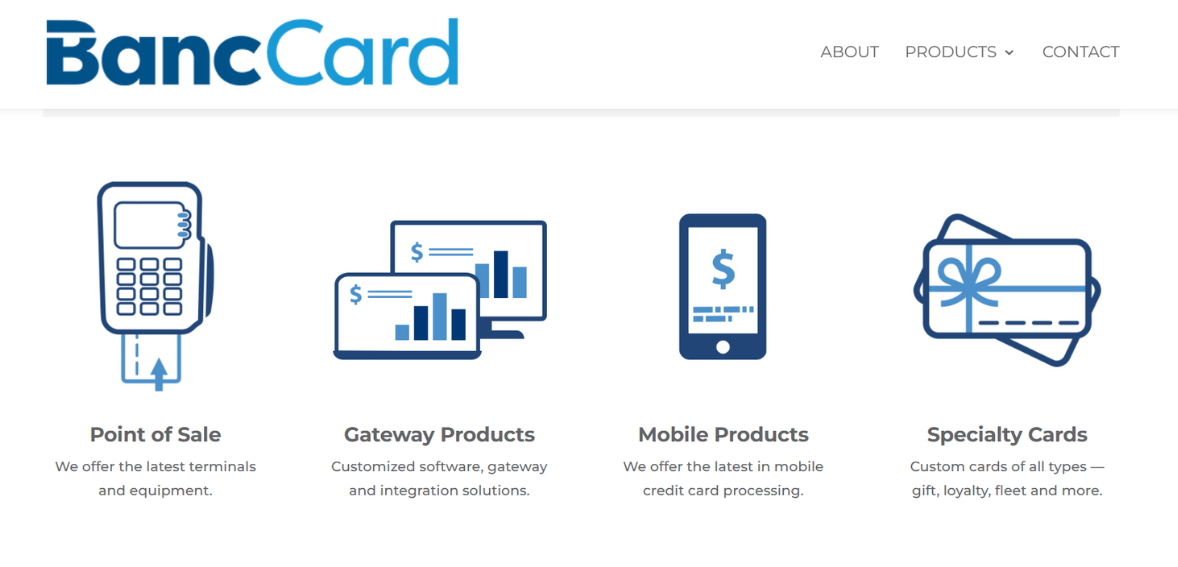

Payment Processing Solutions Offered

BancCard offers full service payment processing for in-person and remote transactions. Their core services include traditional credit and debit card processing, EMV chip cards and contactless payments. This means merchants can serve all types of customers with modern payment methods.

For card-not-present transactions, it supports keyed-in payments, phone orders and recurring billing. They also offer ACH and eCheck processing so businesses have more options beyond card transactions. This makes them good for retailers, service based businesses and even professional service providers like medical offices or non-profits. Mobile payments are also supported through wireless terminals and mobile card readers so merchants can accept payments outside of a fixed retail environment. This is good for delivery businesses, contractors or event vendors who need portability.

As for scalability, BancCard’s solutions are good for small to medium size businesses but may not have the customization of larger processors. They cover the basics well but don’t always compete with enterprise level platforms that have extensive data analytics or advanced fraud prevention suites. For businesses that want reliability and simple payment acceptance, BancCard delivers.

POS Systems and Equipment

BancCard provides access to a variety of point-of-sale systems and card terminals, ensuring merchants can choose equipment that matches their operations. Options typically include countertop terminals for traditional retail environments, wireless terminals for mobile businesses, and integrated POS systems for restaurants or retail chains.

Merchants can also use mobile card readers that connect to smartphones or tablets, giving them flexibility for offsite sales. For businesses that want more advanced systems, it can connect merchants with third-party POS providers that offer features like inventory management, employee scheduling, and customer loyalty programs. While BancCard may not manufacture its own proprietary POS hardware, its partnerships ensure merchants have access to reliable and widely supported equipment.

One important consideration is whether merchants lease or purchase equipment. BancCard offers both models, but leasing can sometimes result in higher long-term costs. Businesses should carefully evaluate these terms before committing. Purchased hardware typically provides better long-term value, but leasing can lower upfront costs, which may appeal to new businesses.

Overall, BancCard’s POS offerings cover the essentials without being overly complex. They are designed for merchants who want straightforward solutions rather than high-tech custom builds. Businesses that require specialized hardware or industry-specific integrations may need to confirm compatibility with BancCard before committing.

E-Commerce and Online Payment Gateway

For merchants who operate online, BancCard offers e-commerce solutions such as virtual terminals and payment gateway integrations. These tools allow businesses to accept card payments through websites, online stores, or invoices. The virtual terminal option is particularly useful for service providers or small businesses that need to process remote payments without a full e-commerce site.

BancCard’s gateway supports recurring billing, tokenization for secure transactions, and compatibility with popular shopping cart systems. This makes it functional for small e-commerce stores as well as subscription-based businesses. However, BancCard’s e-commerce tools are not always as feature-rich as those offered by global providers like Stripe or PayPal, which emphasize developer-friendly APIs and international capabilities.

The platform is sufficient for businesses that primarily serve U.S.-based customers and need a stable, straightforward way to accept online payments. Larger businesses or those with global ambitions may find the features somewhat limited. On the positive side, the gateway is backed by strong security measures and integrates with BancCard’s reporting system, providing businesses with visibility across in-person and online transactions. In essence, BancCard’s e-commerce solutions are solid for local and regional businesses but may not be the ideal choice for high-volume online retailers who require advanced customization and global reach.

Security and Compliance Standards

Security is a key concern in the payments industry, and BancCard emphasizes compliance with PCI DSS standards to protect customer card data. The company provides merchants with guidance on maintaining compliance, which can include annual assessments, network scans, and secure handling of sensitive information.

In addition to PCI DSS, BancCard supports encryption and tokenization, two important technologies that protect cardholder data during transactions. These features reduce the risk of fraud and data breaches, helping merchants safeguard customer trust. Chargeback management tools are also available, giving businesses support in handling disputes and reducing financial exposure.

BancCard’s emphasis on compliance aligns with its banking partnerships, as financial institutions demand high levels of security and adherence to regulations. Merchants working with BancCard may find the compliance requirements more formal compared to some online-first processors, but this structure helps minimize risks in the long term.

While BancCard delivers the basics of payment security effectively, it does not always provide the most advanced fraud prevention suites or AI-driven tools that larger processors are introducing. Businesses that require highly sophisticated fraud detection may need to supplement BancCard’s offerings with third-party tools. Nonetheless, for most small and medium-sized businesses, BancCard’s approach to compliance and security is reliable and sufficient.

Contract Terms and Transparency

One area that merchants consistently evaluate in payment processors is contract structure. It typically operates on multi-year agreements, often with three-year terms. These contracts may include early termination fees if a merchant decides to switch providers before the agreement ends. This structure reflects the company’s more traditional approach, aligning with its bank-driven partnership model.

Merchants should carefully review contract terms to understand monthly fees, service conditions, and cancellation policies. Some reports suggest that early termination fees can be significant, which may be a drawback for businesses that want flexibility. Compared to fintech providers that offer month-to-month agreements, BancCard’s contracts may feel more restrictive.

That said, the benefit of longer-term contracts is often stability in service and pricing. Merchants know what to expect and can rely on the relationship with their local bank partner. For businesses that value predictability and don’t anticipate switching providers, this arrangement can be acceptable.

Transparency around fees is an important consideration. While BancCard is generally upfront about costs through its sales representatives, merchants should still request a full fee disclosure before signing any agreement. Being proactive during contract negotiations helps ensure there are no surprises later.

Pricing Models and Fee Structure

BancCard’s pricing structure typically includes interchange-plus or tiered pricing models, depending on the merchant’s profile and agreement. Interchange-plus pricing is usually more transparent, as merchants pay the actual card network fee plus a fixed markup. Tiered pricing, on the other hand, can make it harder to track true costs, as transactions are grouped into categories with varying rates. In addition to transaction fees, merchants may encounter monthly account fees, statement fees, and costs for PCI compliance. Equipment fees also apply, whether for leased or purchased terminals. Chargeback fees are common across the industry, and BancCard is no exception.

One potential concern is that smaller businesses may face higher relative costs compared to larger merchants with more negotiating power. While BancCard offers competitive rates in many cases, the presence of extra monthly fees may make it less appealing compared to fintech processors that emphasize flat-rate pricing with no monthly charges.

For merchants that value personalized service and long-term banking relationships, BancCard’s pricing may be justified. However, for cost-sensitive businesses or startups, it is important to carefully compare BancCard’s rates with alternatives before committing.

Customer Support and Service Experience

BancCard differentiates itself through its focus on customer support. Many of its services are delivered in partnership with local banks, meaning merchants can often reach out to a trusted community contact for help. This local presence is a strength, as it provides a more personal touch compared to anonymous call centers.

Customer support is available by phone, email, and sometimes through bank partners directly. While not always 24/7, the availability is generally aligned with the needs of small and medium businesses. Reports suggest that responsiveness is a strong point, with representatives providing detailed guidance for troubleshooting and account management.

The tradeoff is that BancCard may not have the same scale of self-service resources or online knowledge bases as larger fintech providers. Merchants who prefer handling issues through online portals or chatbots may find the experience less modern. However, businesses that value direct human support often find BancCard more reliable than some of the larger, impersonal providers.

Ultimately, the customer service experience reflects BancCard’s community-based approach. Businesses looking for a partner that prioritizes relationships and human interaction will likely find its support appealing.

Integration and Compatibility with Business Tools

BancCard offers compatibility with a range of business tools, including accounting software and POS systems. Many merchants integrate BancCard’s processing with platforms like QuickBooks, ensuring streamlined reconciliation of transactions and simplified bookkeeping. For retail and restaurant businesses, integrations with third-party POS providers allow for smooth day-to-day operations. While BancCard itself does not always develop proprietary integrations, its partnerships enable businesses to use widely available software without significant technical barriers.

That said, BancCard’s integration options are not as extensive as those provided by large global processors that invest heavily in developer APIs and customization. Businesses with unique technology stacks or niche requirements may need to confirm compatibility before signing up. For most small and medium businesses, however, BancCard’s integrations are sufficient to cover daily operational needs. The key advantage lies in its ability to balance straightforward functionality with stable support, though it may not be the best fit for enterprises requiring highly customized solutions.

Strengths and Competitive Advantages

BancCard’s primary strengths lie in its relationship-driven model, community partnerships, and reliability. By working closely with local banks, the company builds trust with merchants who already have existing financial relationships. This sets it apart from larger, more impersonal processors that rely heavily on digital-only interactions.

Another advantage is BancCard’s commitment to hands-on support. Small businesses that may feel overlooked by global fintech providers often appreciate the personal attention they receive. In industries where trust and ongoing guidance are crucial, BancCard offers stability and reassurance.

Pricing can also be competitive, particularly for businesses that negotiate favorable interchange-plus agreements. The ability to tailor solutions to the size and needs of a business adds flexibility. Additionally, BancCard’s security and compliance standards meet industry requirements, giving merchants confidence in data protection. These strengths make BancCard a solid choice for businesses that value stability and local connections over cutting-edge features. Its reputation for longevity and reliability reinforces its competitive position.

Limitations and Areas for Improvement

Despite its strengths, BancCard has limitations that potential merchants should consider. The most notable is its reliance on long-term contracts, which can feel restrictive in an era when many competitors offer flexible month-to-month agreements. Early termination fees are a potential drawback for businesses that want adaptability.

Technology is another area where BancCard could improve. While it provides all the necessary tools for payment acceptance, it does not always match the innovation and customization offered by fintech companies. Businesses seeking advanced analytics, global payment acceptance, or developer-friendly APIs may find BancCard lacking.

Additionally, fees such as PCI compliance charges or statement fees can add up, particularly for smaller merchants. Transparency is crucial, and merchants must carefully review contracts to avoid surprises. Finally, the focus on community partnerships, while a strength for some, can also mean that BancCard is not always the best choice for larger enterprises or rapidly scaling online businesses. It serves a specific niche well but may not appeal universally.

Ideal Business Types for BancCard

BancCard is best suited for small to medium-sized businesses that value personal service and banking relationships. Local retailers, restaurants, nonprofits, and service providers benefit most from its community-focused model. These businesses often prefer direct human support and reliable processing over advanced digital tools.

Merchants that already have a relationship with a regional bank partnered with BancCard will likely find the service especially convenient. The ability to manage banking and payment processing through a trusted local partner simplifies operations. On the other hand, businesses that rely heavily on e-commerce, operate internationally, or require advanced technological customization may find BancCard less suitable. In those cases, global fintech providers with broader capabilities may be better fits. Overall, it works well for traditional businesses that prioritize trust, relationship-based service, and stability over trend-driven features.

Final Verdict: Is BancCard Worth It?

It offers a relationship-focused approach to payment processing, ideal for merchants who value personal service and partnerships with local banks. It provides essential solutions like card processing, POS systems, online payments, and compliance support with reliability and security. However, its multi-year contracts, possible hidden fees, and limited innovation may not suit e-commerce or fast-growing businesses. While local retailers and small service providers benefit from its personal support, those seeking advanced fintech tools and flexibility may prefer options like Stripe, Square, or PayPal. Overall, it suits businesses prioritizing community connections, provided they understand all contract and fee details.

FAQs

Q1: Does BancCard support high-risk merchants?

It primarily focuses on low-to-medium-risk industries. While it offers solid support for mainstream businesses, high-risk merchants may find approvals difficult or be directed to specialized processors.

Q2: What is the main difference between BancCard and larger processors like Stripe or Square?

The biggest difference is BancCard’s relationship-driven model. It emphasizes partnerships with local banks and personal service, while larger processors focus more on technology, automation, and global reach.

Q3: Are there hidden fees with BancCard’s services?

Merchants may encounter extra costs such as PCI compliance fees or statement fees, depending on their contract. While BancCard provides transparency through its representatives, merchants should carefully review agreements to ensure clarity on all charges.