Blog

Home / Blog

Priority Payment Systems Review

- 21st Apr, 2026

- | By Linda Mae

- | Reviews

Priority Payment Systems has traveled a considerable distance from its origins as a traditional merchant credit card processor. Founded in 2005 and headquartered in Alpharetta, Georgia, the company has grown through a series of strategic acquisitions and rebranding exercises into Priority Technology Holdings, Inc., a publicly traded payments and financial technology company listed on NASDAQ under the ticker PRTH. What began as a regional merchant services provider now operates at genuine scale, serving over 800,000 clients and processing more than $115 billion in annual payments volume. Lets read more about Priority Payment Systems Review.

The company’s evolution reflects a deliberate strategy to move beyond basic payment acceptance toward what it calls a Unified Commerce Platform, combining merchant acquiring, banking as a service, B2B payments, and embedded finance capabilities under one technology roof. Key milestones include a 2014 merger with Cynergy Data, a 2021 acquisition of Finxera to add banking-as-a-service functionality, and a 2023 acquisition of Plastiq, the B2B bill pay and working capital platform, which significantly expanded Priority’s reach into business spend management.

Table of Contents

ToggleCompany Background and Market Position | Priority Payment Systems Review

Priority Payment Systems was launched in 2005 by Thomas Priore, who continues to serve as Chairman and CEO. The company’s early years were focused on building a traditional merchant acquiring business before a series of strategic moves transformed it into something considerably more ambitious. The 2013 partnership with TSYS for payment processing services provided a solid backend foundation. The 2014 merger with Cynergy Data, a New York-based processor, expanded Priority’s merchant portfolio and geographic reach significantly, and the combined entity was restructured as Priority Holdings, LLC.

The company went public in 2018 on NASDAQ, providing access to capital that accelerated its acquisition strategy. The 2021 acquisition of Finxera added banking-as-a-service infrastructure, enabling Priority to offer embedded banking, stored value accounts, and card issuing capabilities alongside its existing payments platform. The 2023 acquisition of Plastiq added B2B bill pay and working capital tools to the portfolio. The combined entity now operates as Priority Technology Holdings, Inc. and markets its full offering under the Priority Commerce brand.

Priority competes in several overlapping markets simultaneously: traditional merchant services for SMBs, integrated payments for ISVs and software platforms, B2B commercial payments, and banking-as-a-service for enterprise clients. This breadth is a genuine differentiator relative to single-focus processors, but it also means the platform’s quality and relevance varies considerably depending on which segment of its offering a given merchant actually needs.

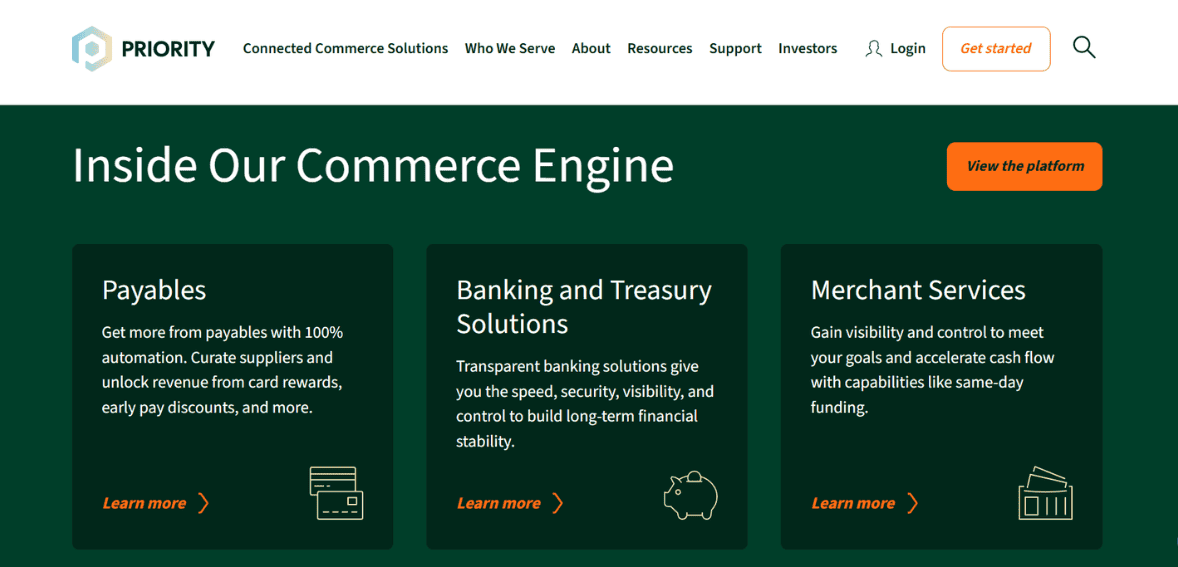

Core Payment Processing Capabilities

At its foundation, Priority Payment Systems provides full-service merchant acquiring across credit cards, debit cards, and ACH payments. The company operates as a non-bank merchant acquirer, meaning it handles the complete transaction lifecycle including authorization, clearing, settlement, and funding directly rather than routing through a third-party acquirer for every transaction. This ownership of the acquiring relationship gives Priority greater control over the merchant experience and more flexibility in pricing and feature customization.

It processes all major network transactions from cards such as Visa, MasterCard, American Express, and Discover. Transactions on ACH networks are processed by Priority Payment Systems; this process is especially useful for B2B merchants, for companies that have recurring transactions, and merchants with high-volume transactions in which card processing costs are too much compared to the volume of the transaction.

The backend processing platform from Priority Payment systems is based on MX Merchant platform where merchant management takes place. Since this platform manages everything related to payment processing, reports, invoices, and tools used by businesses will all be found in one platform rather than several. The size of the payment processing platform, over $115 billion per year through over 800,000 clients, shows that the company has real infrastructure depth. It means merchants can trust that the underlying payment processing platform has been tested extensively and will handle their transactions without any issue.

The MX Merchant Platform

MX Merchant is Priority’s flagship technology product and the centerpiece of its merchant-facing offering. It is an integrated payment processing and business management system designed to consolidate transaction management, invoicing, recurring billing, customer data, and reporting into a single platform. Understanding MX Merchant is essential to evaluating whether Priority is the right fit for a given business.

The platform is organized into several functional modules. MX Storefront is an eCommerce tool that enables merchants to accept payments online and build a digital storefront within the MX ecosystem. MX Express is an iOS mobile app for card acceptance on the go, supporting tips, voids, returns, and digital receipts from a smartphone. MX Invoicing handles invoice generation, recurring payment scheduling, and payment tracking. MX Insights is an analytics tool that provides transaction data analysis, competitive benchmarking, and cardholder demographic insights, making it one of the more distinctive features in Priority’s stack.

The platform is customizable, which allows it to be configured to the specific needs of different business types and industries. This flexibility is genuinely valuable for businesses with non-standard workflows or those operating across multiple sales channels. However, merchants should be aware that MX Merchant is also licensed to other payment processors as a white-label platform. This means that the product is sold and supported through multiple channels, and the quality of support and configuration assistance can vary significantly depending on which reseller or ISO a merchant is working with.

POS Systems and Hardware

Priority Payment Systems offers a range of POS hardware and software solutions targeted at different business environments. The hardware lineup includes terminals and POS systems from established manufacturers including Poynt, Ingenico, Clover, and PAX Technologies, giving merchants a variety of options depending on their preference for functionality, form factor, and price point.

Clover, which is widely regarded as one of the stronger POS platforms in the SMB market, is available through Priority’s offering. Clover’s app marketplace allows merchants to extend the functionality of their POS system with third-party integrations for inventory management, loyalty programs, staff scheduling, and other operational tools. However, as with any Clover deployment, merchants should understand that the Clover ecosystem is not compatible with other hardware brands, meaning hardware flexibility is limited once a Clover system is in place.

In particular for the restaurant business, Priority provides special POS setups which facilitate table management, online ordering via the e-tab solution, and kitchen display capabilities. Retail merchants benefit from inventory control and sales tracking features through the POS level. The possibility to integrate POS equipment with the back-end of the MX Merchant solution allows for a link between the merchant’s transactions, reports, and client management tools.

Merchants are advised to pay special attention to the hardware costs either through buying outright or through leasing. It seems that equipment leasing in the merchant services space has traditionally been a matter of controversy with many merchants locked into multi-year leases on hardware equipment which could be purchased more cheaply outright.

Passport: Banking as a Service for SMBs

One of Priority’s more distinctive offerings relative to traditional payment processors is the Passport product, a banking-as-a-service solution designed specifically for SMB merchants. Passport transforms Priority’s role from payment processor into a broader financial services partner, offering merchants faster access to funds, corporate debit cards for employees, vendor payment capabilities, interest-bearing savings accounts, and money market accounts, all within the Priority platform.

The faster funding component is particularly relevant for cash-flow-sensitive small businesses. Rather than waiting for the standard one-to-two business day settlement cycle, Passport allows merchants to access funds more quickly, reducing the gap between when a sale is made and when the money is available for business use. For businesses operating on tight working capital, this can be a meaningful operational advantage.

Corporate debit cards issued through Passport give business owners a way to manage employee spending without needing a separate business banking relationship for that function. Vendor payment capabilities within the same platform further reduce the number of financial tools a merchant needs to manage simultaneously.

The Passport offering reflects Priority’s strategic direction as a unified commerce platform rather than a narrow payment processor. For merchants who want to consolidate more of their financial operations with a single provider, Passport represents genuine added value. That said, merchants should evaluate the specific terms, interest rates, and fees associated with Passport accounts relative to dedicated business banking products before treating it as a complete substitute for a traditional business bank account.

Plastiq and B2B Payment Capabilities

Priority’s 2023 acquisition of Plastiq significantly expanded its B2B payments capabilities and brought a new dimension to what the platform can offer businesses managing vendor relationships and working capital. Plastiq was originally built to solve a specific and common problem: many businesses want to pay suppliers by credit card to earn rewards and preserve cash, but most suppliers only accept checks or ACH. Plastiq bridges that gap.

With Plastiq Pay, businesses will be able to use credit cards to pay suppliers that do not accept cards as a form of payment. Using the service provided by Plastiq, the actual payment will be made through the preferred medium used by the supplier; however, the business will charge its credit card and enjoy the benefits associated with the payment terms and rewards from its credit card. For businesses that make payments to suppliers through vendor spend, there is no doubt that they will enjoy improved cash flow management as a result.

Through Plastiq Accept, businesses will have the ability to accept payments through credit card and avoid paying merchant fees on their own through the fee passthrough method. The suite of API available for Plastiq Connect extends Plastiq’s services to marketplaces, platforms, and enterprise resource planning platforms.

Plastiq’s inclusion into the priority platform makes Priority capable of handling finance teams for growing companies that require better solutions in accounts payable and receivable rather than just payment solutions. The company has indeed expanded its market, but it will probably take time before its merchants fully recognize the value of Plastiq.

Specialized Industry Solutions

Beyond its general merchant services offering, Priority Payment Systems has built several specialized products targeting specific industries, which is worth understanding separately because these vertical tools can represent meaningful added value for businesses in the relevant sectors.

LandlordStation is a payment solution designed specifically for property managers and landlords, enabling online rent collection, tenant payment portals, and lease management tools integrated with the payment processing layer. For property management businesses that deal with high volumes of recurring monthly payments from tenants, having a purpose-built payment tool rather than a generic invoicing system can meaningfully reduce administrative friction.

PayRight is a healthcare-specific payment management system that aims to handle billing, co-pay, and recurring payments for their clients. Considering how complicated the billing process is in healthcare and the need for a convenient way of paying, a dedicated solution would be more efficient than the conventional merchant terminal.

Moreover, e-tab allows restaurants to conduct online orders from their website through which the customer can choose meals from the menu and place an order with payment. The relevance of such an option has increased greatly during and after the acceleration of online ordering trends in the pandemic era. As a result, Priority’s restaurant merchants would have an advantage over other companies using third-party ordering systems.

Finally, CBD payment solutions are offered as a niche product that is important for Priority to pursue. This service becomes important because traditional processors often refuse or restrict merchant accounts of CBD-related companies. Thus, having an open approach toward serving this segment, provided there is no risk involved, will allow Priority to capitalize on its advantage over competitors.

Pricing Structure and Fees

Pricing at Priority Payment Systems follows the pattern common across most traditional merchant services providers: rates are customized per merchant, not published publicly, and require direct engagement with a sales representative to obtain a quote. This lack of upfront transparency is a recurring criticism from merchants evaluating the platform, and it creates real friction for businesses trying to compare processors without committing to a sales conversation.

Priority does offer interchange-plus pricing, which is the more transparent and generally more merchant-favorable pricing model compared to tiered pricing. Under interchange-plus, the actual card network interchange cost is passed through at cost, and the merchant pays a fixed markup on top of that. Independent reviewers with access to Priority statements have reported markups ranging from approximately 0.12% plus $0.10 per transaction for high-volume merchants processing $300,000 or more monthly, to 0.40% plus $0.02 per transaction at lower volumes. American Express transactions have been observed at markups as high as 0.60% plus $0.02 per transaction.

Additional fees apply across various categories including monthly service fees, statement fees, batch fees, and PCI compliance fees. Early termination fees are a standard feature of Priority contracts, and the three-year contract term that appears to be standard creates meaningful commitment risk if the relationship does not work out as expected. Merchants should request a comprehensive fee schedule in writing before signing, specifically asking about monthly minimums, annual fees, and any fees associated with specific features or integrations they plan to use.

Contract Terms and Merchant Agreements

Contract terms at Priority Payment Systems have been a consistent source of merchant complaints, and this area requires careful attention during the evaluation and sign-up process. The standard contract length appears to be three years, with early termination fees applying if a merchant exits the agreement before the term ends. Automatic renewal provisions are common in the industry and should be specifically identified and understood before signing.

The use of independent sales organizations and agents to sell Priority’s services introduces variability into the onboarding process. Merchants whose accounts are set up through a third-party ISO or agent may find that cancellations, billing disputes, or account changes require navigation through both the agent and Priority directly, which can create confusion about accountability and extend resolution timelines. BBB complaints for Priority frequently involve situations where a merchant believed they had canceled their account through an agent, only to discover that Priority continued billing because the cancellation was not properly processed.

In May 2025, Priority Technology Holdings and a partner agreed to a $19.5 million settlement to resolve a class action lawsuit in California related to telephone solicitations. The case alleged that a third-party sales agent recorded sales calls without consent, affecting nearly 19,000 businesses in California. While Priority denied direct wrongdoing and settled to avoid prolonged litigation, the case illustrates the legal exposure that can arise from a distributed, agent-based sales model where oversight of third-party conduct is incomplete.

Merchants should request all contract documents before signing, identify the cancellation process and required notice period in writing, confirm early termination fee amounts, and establish direct contact with Priority’s corporate support team rather than relying solely on their sales agent for account management.

Security and Compliance

Priority Payment Systems takes a comprehensive approach to payment security, covering the core requirements merchants need to protect cardholder data and maintain compliance with industry standards. The platform’s security infrastructure operates under the ControlScan PCI compliance management system, which provides merchants with tools and support for meeting Payment Card Industry Data Security Standard requirements.

ControlScan is available through Priority as a marketplace application and includes direct compliance consultations, PCI compliance tools, and ongoing support for the compliance process. For smaller merchants who lack dedicated IT or security resources, having structured compliance assistance integrated into the payment relationship is a practical benefit that reduces the risk of inadvertent non-compliance.

Encryption and tokenization are standard features of the platform’s transaction processing, ensuring that sensitive cardholder data is protected both in transit and at rest. These measures are foundational to any modern payment security architecture and represent the minimum expectation for any processor handling card data at scale.

Priority’s proprietary processing solutions are supported by nationwide money transmission licenses and include automated risk management, underwriting, and full AML, BSA, and OFAC compliance infrastructure. This regulatory coverage is particularly relevant for merchants using the Passport banking-as-a-service features, where the obligations extend beyond standard payment security into broader financial compliance.

Merchants in industries with elevated fraud risk should discuss the specific fraud monitoring and chargeback management tools available to their account type before assuming that the standard security package meets their exposure level.

Reporting and Analytics

One of the more differentiating aspects of Priority’s platform relative to basic merchant processors is the depth of its reporting and analytics capabilities, primarily delivered through the MX Insights component of the MX Merchant suite. MX Insights goes beyond standard transaction reporting to offer competitive benchmarking, cardholder demographic analysis, and spending pattern data, tools that are typically reserved for enterprise-level platforms.

For SMB merchants, having access to this kind of data within the same platform used for daily payment processing is genuinely useful. Understanding how your customer base compares to competitors in the same geography or category, what demographics are driving revenue, and how transaction patterns change seasonally can inform business decisions that go well beyond payment management. This positions MX Insights as a business intelligence tool, not merely a reconciliation aid.

Standard reporting features cover transaction history, settlement summaries, batch reports, and chargeback tracking. These operational reports meet the day-to-day accounting and reconciliation needs most merchants encounter. The merchant portal provides 24/7 access to account activity, and report customization allows merchants to filter data by date range, transaction type, and other parameters.

For merchants using multiple Priority products across the Passport, Plastiq, and MX Merchant layers, consolidated reporting across these functions remains an area to verify specifically, since multi-product deployments can create data silos that require active management to keep aligned.

Customer Support

Customer support at Priority Payment Systems presents a pattern familiar from the broader merchant services industry: institutional capability exists at the corporate level, but the experience an individual merchant actually receives varies considerably depending on how their account was established and who is responsible for ongoing service.

Priority offers 24/7 customer support through its corporate service channels, and the company has received industry recognition for its call center operations. For merchants with direct corporate relationships, particularly those in higher-volume tiers or with specialized industry integrations, the support experience tends to be more responsive and more technically capable.

The challenge lies in Priority’s distributed sales model. Merchants onboarded through independent sales organizations or resellers often find that their primary support relationship is with the ISO or agent rather than with Priority directly. When issues arise involving billing disputes, account cancellations, or equipment problems, the handoff between the agent and Priority’s corporate team can be slow and frustrating. BBB complaints frequently describe merchants who spent weeks or months trying to resolve cancellation-related issues because neither the agent nor Priority’s corporate team took clear ownership of the problem.

Positive reviews, including those from the Priority Payments Local branch, highlight the value of being assigned a dedicated account representative who responds quickly and consistently. This level of service is achievable within the Priority ecosystem but is not uniformly guaranteed across the full merchant base. Merchants evaluating Priority should ask specifically about who their primary support contact will be post-sale and what the direct escalation path to Priority’s corporate team looks like before committing.

Strengths, Limitations, and Who It’s Best For

Priority Payment Systems has evolved into a genuinely comprehensive payments and financial technology platform that offers more than most traditional merchant processors. The MX Merchant platform is well-designed and feature-rich, the Passport banking-as-a-service offering adds real value for cash-flow-focused SMBs, the Plastiq acquisition has meaningfully extended B2B capabilities, and the vertical-specific tools for landlords, healthcare providers, and restaurants show real investment in industry-relevant solutions. Processing scale, interchange-plus pricing availability, and publicly traded corporate governance are all positive markers.

The limitations are equally real. Pricing transparency requires direct sales engagement, which creates friction in the evaluation process. The three-year contract with early termination fees represents significant commitment risk. The distributed sales model through ISOs and independent agents creates uneven merchant experiences, and the volume of complaints around difficult cancellations and unexpected fees is a consistent pattern across independent review platforms. The 2025 California class action settlement, while resolved without admission of wrongdoing, reinforces the concern that third-party sales practices have not always aligned with the standards that corporate-level operations promote.

The merchants best positioned to benefit from Priority Payment Systems are those with higher processing volumes who can negotiate favorable interchange-plus rates, businesses in the vertical markets where Priority has built specialized tools, ISVs and software companies seeking an embedded payments partner through the Passport API layer, and B2B-focused businesses that can leverage the Plastiq integration for vendor payment management. Merchants with simpler needs or those prioritizing pricing transparency and contract flexibility may find more straightforward value elsewhere.

FAQs

Q1. What is the difference between Priority Payment Systems and Priority Technology Holdings, and does it matter which entity a merchant is dealing with?

Priority Payment Systems is the original merchant services brand, founded in 2005, which subsequently became Priority Technology Holdings, Inc. (NASDAQ: PRTH) following a series of acquisitions and a 2018 public listing. The merchant-facing brand now operates as Priority Commerce. For most merchants, the entity they interact with for payment processing is the Priority Payment Systems division, which functions as the acquiring and merchant services arm within the broader Priority Technology Holdings structure.

The distinction matters primarily in the context of understanding what products are available. The full suite, including Passport banking services and Plastiq B2B payment tools, sits within Priority Technology Holdings, while the core acquiring and MX Merchant products have historically been the domain of the Priority Payment Systems business unit. Merchants should clarify with their account representative exactly which products are included in their agreement and which entity is responsible for delivering each component of the service.

Q2. How does Priority Payment Systems pricing compare to other processors, and is there room to negotiate?

Priority does offer interchange-plus pricing, which is generally considered more transparent and cost-effective than tiered pricing models used by many competing processors. Independent analysis of Priority statements suggests that markup rates for high-volume merchants can be quite competitive, while lower-volume merchants tend to pay higher markups. Pricing is not published and requires direct negotiation with a sales representative, which means the rate a merchant receives depends significantly on their volume, business type, and the specific ISO or sales channel they engage through. There is room to negotiate, particularly on the markup percentage, monthly fees, and early termination terms.

Merchants should obtain quotes from multiple processors before committing, request a full written fee breakdown rather than just the headline rate, and specifically ask about American Express transaction pricing, which has been observed at higher markups than Visa and Mastercard rates.

Q3. What should merchants know about canceling a Priority Payment Systems contract?

Canceling a Priority Payment Systems contract requires careful attention to the process and timing. Standard contracts appear to include a three-year term with an early termination fee, and automatic renewal provisions mean that failing to provide timely written notice before the contract renewal date can lock a merchant into another term. The required notice period should be specified in the contract and should be calendared well in advance.

Cancellation requests should be submitted in writing directly to Priority’s corporate customer service team, not solely through a sales agent or ISO, as agent-mediated cancellations have been a source of disputes where the cancellation was not processed correctly. Merchants should request written confirmation of cancellation, confirm that all automatic billing has stopped, and monitor their bank account for continued charges after the cancellation date. If unauthorized charges continue after confirmed cancellation, the appropriate steps include disputing the charges with your bank and filing a complaint with the Consumer Financial Protection Bureau if the issue is not resolved promptly.