Blog

Home / Blog

FortisPay Review

- 24th Dec, 2025

- | By Linda Mae

- | Reviews

FortisPay markets itself as a full-service payment processing solution intended to accommodate businesses with flexibility in mind, from physical, e-commerce, and subscription payments. Like most contemporary payment processing solutions, the promised benefit lies in the ability to simplify payment processing methodologies for businesses in addition to being equipped with features and services not typically associated with payment agreements. Businesses choosing FortisPay would be seeking consistency in their operations. Lets read more about FortisPay Review.

The reason to review FortisPay in-depth is because it offers solutions that are centered on operational reliability rather than just being a solutions-oriented processor that businesses might not necessarily need. Rather, this processor seems to focus on businesses that are in need of reliable processing services, standard onboarding services, and those that require extended payment solutions in one provider rather than several.

However, FortisPay competes in an area where there are many options. It is important to understand how companies such as FortisPay deal with issues of price, compliance, risk, and integrations before making a decision. It’s worth taking the time to review FinTech companies and how they address the above issues to find the best solution.

Table of Contents

ToggleOverview of FortisPay’s Core Payment Processing Capabilities | FortisPay Review

At its core, FortisPay provides standard merchant account services that allow businesses to accept card-present and card-not-present payments. Transactions are routed through established payment networks, with settlement handled on a regular funding schedule. From an operational standpoint, FortisPay functions much like a traditional processor rather than a lightweight payment facilitator, which can influence underwriting depth and account stability.

Merchants using FortisPay typically gain access to tools for authorizing payments, managing refunds, and handling charge adjustments through a centralized system. The platform focuses on maintaining consistent uptime and transaction reliability, which is often more important to established businesses than experimental features. Processing speeds and authorization flows are generally aligned with industry norms, meaning FortisPay does not reinvent payment mechanics but aims to execute them reliably.

One aspect worth noting is that FortisPay’s processing environment is designed to support multiple business models. Whether payments occur in a physical location, through remote orders, or via recurring billing, the underlying infrastructure remains unified. This reduces fragmentation for businesses operating across channels. However, merchants should understand that with this structure often comes more formal underwriting and compliance expectations compared to plug-and-play platforms. For businesses prepared for that level of structure, FortisPay’s core processing capabilities can offer consistency and control rather than shortcuts.

Supported Payment Methods and Card Networks

FortisPay supports the major credit and debit card networks that most businesses expect, ensuring compatibility with common consumer payment habits. This includes standard card-present transactions as well as card-not-present payments for phone, mail, and online orders. For many merchants, this baseline coverage is sufficient and aligns with daily transaction needs.

Beyond cards, FortisPay also supports ACH payments, which can be valuable for businesses handling recurring invoices, large ticket transactions, or B2B payments where bank transfers are preferred. ACH acceptance can help reduce processing costs compared to card payments, though it also introduces different settlement timelines and return risks that businesses must manage.

The platform’s approach to payment methods emphasizes reliability over experimentation. While some processors aggressively push newer digital wallets or alternative payment methods, FortisPay appears to prioritize stable, widely adopted options. This may feel conservative to merchants seeking cutting-edge payment trends, but it can be reassuring for businesses that value predictability and lower operational risk.

It is important for merchants to confirm which payment methods are enabled by default and which may require additional setup or underwriting approval. Not every account configuration is identical, and supported payment methods can vary based on business type and risk profile. Overall, FortisPay covers the essentials well, but businesses seeking extensive alternative payment ecosystems should review compatibility carefully.

Pricing Structure and Fee Transparency

Pricing is one of the most critical factors when evaluating FortisPay, and like many traditional processors, its structure may not be immediately visible upfront. Fees typically include processing rates, transaction fees, monthly account costs, and potential compliance-related charges. This layered pricing approach is common in the industry but requires careful review to avoid surprises.

FortisPay does not position itself as a flat-rate or instant-signup provider. Instead, pricing is often customized based on business volume, transaction types, and risk considerations. This can work in a merchant’s favor if rates are negotiated properly, especially for businesses with consistent processing volumes. However, smaller merchants or those unfamiliar with payment pricing should take time to understand how rates are calculated and where additional fees may apply.

Transparency largely depends on how clearly terms are communicated during onboarding. Merchants should review statements, contracts, and fee schedules closely before signing. Questions around early termination fees, monthly minimums, and PCI compliance charges should be addressed upfront. FortisPay’s pricing model is not inherently problematic, but it does require attention and due diligence.

For businesses that value tailored pricing and are willing to engage in negotiation, FortisPay’s approach can be reasonable. For those seeking instant clarity without conversation, the pricing structure may feel less accessible.

Hardware and POS Compatibility

FortisPay also supports different payment terminals and point-of-sale solutions to suit the business environment of the clients. There are countertop terminals for retail businesses, wireless readers for businesses that operate while on the move, and virtual terminals for offsite businesses. This is crucial for organizations that conduct operations in different environments.

Instead of binding merchants to devices that are only available from their own companies, FortisPay usually partners with already existing terminal providers. This can help solve the hardware issues that were prevalent with old solutions. Also, the ability to integrate with third-party POS solutions means that existing business processes are not discarded.

However, not all other hardware configurations are universal, so merchants need to check compatibility with providers. Additionally, certain point-of-sale systems might need other forms of integration or do not necessarily offer all of the universal features of FortisPay. Even hardware purchases or leases might vary, such as for devices, which would affect long-term budgets. In general, FortisPay’s hardware and point-of-sale solution is functional as opposed to restrictive. It can handle various business requirements without being overly complicated, though one ought to confirm whether their configuration supports FortisPay’s compatible system.

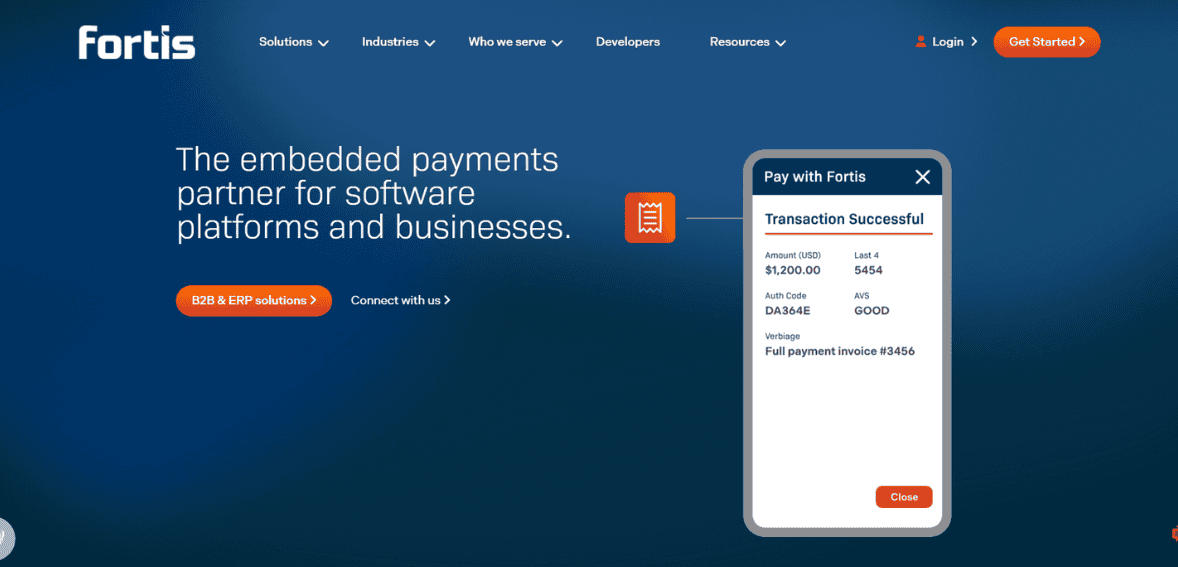

Virtual Terminal and Online Payment Tools

FortisPay offers virtual terminal functionality that allows merchants to process payments through a web-based interface. This is especially useful for businesses that accept phone or email orders, manage invoices, or operate without a traditional storefront. The virtual terminal typically supports card entry, transaction history access, and basic reporting.

Online payment tools extend this functionality to ecommerce and remote payment acceptance. Depending on configuration, businesses can integrate FortisPay into websites or use hosted payment pages to reduce compliance burdens. These tools are designed to balance usability with security, making them suitable for businesses that want online payments without building custom systems.

While FortisPay’s online tools are functional, they are not necessarily designed to compete with developer-centric platforms focused on deep customization. Instead, they aim to provide reliable payment acceptance with straightforward setup. This approach suits businesses that prioritize operational stability over advanced frontend control.

Merchants should evaluate whether FortisPay’s online tools align with their growth plans. For basic ecommerce and remote payments, they are generally sufficient. For highly customized online experiences, additional development resources or integrations may be required.

Recurring Billing and Subscription Management

Recurring billing is highly important in subscription models, membership, and service-based business. FortisPay enables you to set up recurring payments; it allows merchants to automate billing schedules and securely store payment credentials. This can reduce a lot of manual work and might improve cash flow consistency.

Billing schedules, customer profiles, and failed payments in most instances are also managed by the recurring billing tools. Operationally, this level of automation can seriously reduce administrative overhead. It minimizes missed payments when appropriately set up.

However, recurring billing also means more responsibility for customer communication and regulatory compliance. Merchants are supposed to make sure customers understand how they will handle the terms of the bills and that stored payment information is securely handled. FortisPay tools support these needs, but success depends on how well businesses manage setup and ongoing monitoring.

Businesses dependent on subscriptions will need to test the workflows for recurring billings in detail prior to scaling. While FortisPay provides the infrastructure for this, the merchant is still responsible regarding customer experience and accuracy of billing.

Security Standards and Compliance Support

Security and compliance are central to FortisPay’s value proposition. The platform supports PCI compliance requirements and uses encryption to protect sensitive payment data. These measures are essential for reducing exposure to data breaches and fraud.

FortisPay typically provides guidance on compliance responsibilities, but merchants should understand that compliance is a shared obligation. Tools and support can simplify the process, but businesses must still follow best practices and complete required validations. Failure to do so can result in additional fees or account issues.

Fraud prevention tools may include basic monitoring and transaction controls, though these features vary by account type. Businesses operating in higher-risk environments should clarify what protections are included and whether additional services are available. Overall, FortisPay’s security approach aligns with industry expectations. It is neither minimal nor overly complex, but merchants must engage actively with compliance requirements to maintain account health.

Reporting, Dashboards, and Transaction Insights

FortisPay provides reporting tools that allow merchants to view transaction history, settlements, and basic performance metrics. These dashboards are designed to support day-to-day reconciliation rather than advanced analytics. For many businesses, this level of reporting is sufficient to track revenue and identify issues.

Reports typically include transaction summaries, batch details, and funding information. Access to this data helps merchants resolve disputes, manage refunds, and understand cash flow timing. The interface focuses on clarity and function rather than visual complexity. Businesses seeking deep analytics or predictive insights may find reporting somewhat limited. However, for operational management and accounting alignment, FortisPay’s reporting tools perform their role effectively. Integration with external accounting systems can further extend reporting capabilities.

Integration Options and API Accessibility

FortisPay supports integrations with select ecommerce platforms, accounting tools, and POS systems. These integrations reduce manual data entry and help maintain consistency across systems. For many merchants, prebuilt integrations are sufficient and simplify implementation.

API access may be available for businesses that require custom workflows. This allows developers to connect FortisPay to proprietary systems or unique operational setups. However, API-based integration requires technical resources and should be evaluated carefully. FortisPay’s integration strategy emphasizes stability over experimentation. Businesses with standard integration needs will likely find adequate support, while highly customized environments may require additional planning.

Customer Support and Merchant Onboarding Experience

Onboarding and support can significantly influence a merchant’s long-term experience. FortisPay typically offers guided onboarding, which can help reduce setup errors and ensure compliance requirements are met. This structured approach may feel slower than instant signup platforms but can improve account stability.

Customer support responsiveness varies by account configuration, but access to knowledgeable representatives is a key expectation. Merchants should clarify support channels, response times, and escalation processes before onboarding. A structured onboarding process can be a strength for businesses that value guidance. However, those seeking immediate activation may need to adjust expectations.

Contract Terms, Account Stability, and Risk Policies

FortisPay operates with formal contracts that outline terms, fees, and termination conditions. Merchants should review these documents carefully, paying attention to contract length, early termination fees, and reserve policies. Account stability is influenced by underwriting and ongoing monitoring. FortisPay’s risk management approach aims to reduce sudden disruptions, but merchants must maintain transparent operations and communication. Understanding risk policies upfront can help prevent surprises. FortisPay’s structure favors businesses that value predictability and compliance.

Pros of Using FortisPay

It offers reliable processing, multi-channel support, and structured onboarding. Its focus on stability and compliance can benefit established businesses seeking consistency.

Potential Limitations and Considerations

Pricing complexity, formal contracts, and limited cutting-edge features may not suit every business. Merchants should weigh these factors carefully.

Ideal Business Types for FortisPay

It is best suited for small to mid-sized businesses, service providers, and merchants seeking dependable, long-term payment infrastructure.

FAQs

Is FortisPay suitable for small and growing businesses?

Yes, particularly for businesses prepared for structured onboarding and formal contracts.

Does FortisPay support both in-person and online payments?

Yes, it supports card-present, online, and recurring payment environments.

How transparent is FortisPay when it comes to fees and contracts?

Transparency depends on careful review and clear communication during onboarding.