GoCardless Review

- 06th Jun, 2025

- | By Linda Mae

- | Reviews

GoCardless is a London-based fintech company that specializes in bank-to-bank payments, primarily through Direct Debit systems. Founded in 2011, it has carved out a space for itself as a cost-effective alternative to traditional card payment processors. Rather than relying on card networks like Visa or Mastercard, GoCardless enables businesses to collect payments directly from their customers’ bank accounts. This approach is especially attractive to companies dealing with recurring payments such as subscriptions, memberships, or invoice-based billing. Lets read more about GoCardless Review.

With operations in more than 30 nations and multi-currency payment support, GoCardless caters to a wide range of international customers. Its infrastructure is made to make payment collection easier for both big and small businesses. It has gained popularity over time among a variety of industries, including nonprofits, accounting services, gyms, and SaaS platforms.

The platform’s emphasis on decreasing manual follow-ups and payment failures; common problems in subscription and invoice-driven models; is one of its main advantages. GoCardless wants to give businesses better predictability and higher conversion rates by utilising automated payment flows and bank authentication systems.

Although not as widely known among consumers as some card-based systems, GoCardless operates behind the scenes, making the payment process more seamless. It’s important to note that this system works best when both payer and payee are comfortable with bank debits, which might not always suit all customer segments.

Core Payment Features and Capabilities | GoCardless Review

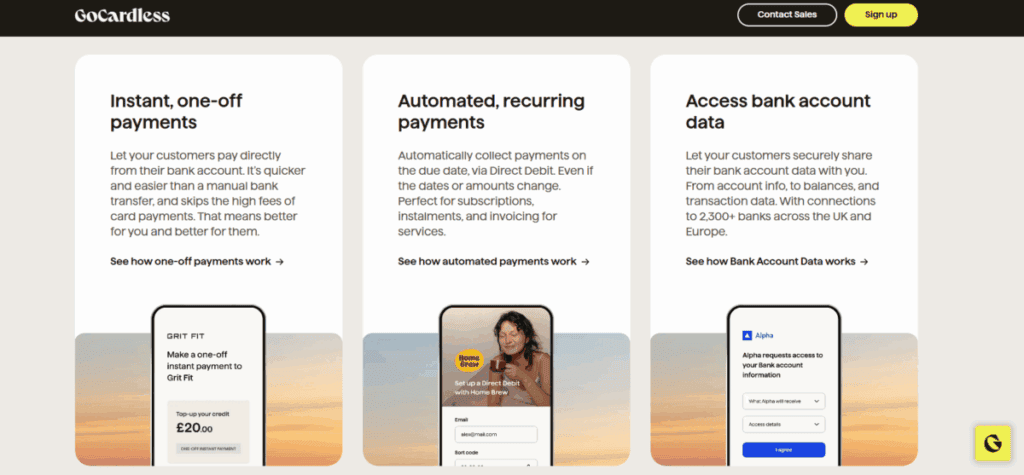

GoCardless centers its payment processing around bank debit, which can be more reliable and cost-effective than credit or debit card processing for specific business models. The primary service is Direct Debit, allowing businesses to pull funds from a customer’s bank account with authorization. This is particularly well-suited for recurring transactions such as monthly memberships, subscriptions, or installment plans.

In addition to recurring payments, GoCardless supports one-off transactions, though it is not as frequently used for this purpose compared to card processors. One of its notable innovations is Instant Bank Pay, which leverages open banking to enable real-time, one-time payments. This addresses a key limitation of traditional Direct Debit, which typically involves a delay of a few days for processing.

Another strength is GoCardless’s ability to automatically retry failed payments, reducing the burden on finance teams. It also allows for customizable payment pages, automatic notifications, and full control over customer mandates. Users can set up billing schedules, view payment statuses, and manage customers all in one place.

GoCardless supports multiple currencies, including GBP, EUR, USD, AUD, and NZD, and continues to expand its international capabilities. While it’s an excellent tool for subscription-first businesses, it is less suitable for industries that rely heavily on real-time authorization or point-of-sale needs. In summary, GoCardless offers a robust set of features tailored for recurring and account-based billing, though it remains more niche in areas dominated by card payments or cash-on-delivery models.

Integration and API Flexibility

One of GoCardless’s strongest selling points is its API, designed for developers looking to build custom payment solutions. It offers a clean, RESTful interface and supports webhooks to keep systems synchronized in real time. This is particularly valuable for SaaS platforms and digital-first businesses that need to tightly integrate payment flows within their own products.

GoCardless is developer-friendly since it offers a test environment, SDKs in multiple programming languages, and extensive documentation. With little manual involvement, companies with internal technical teams can automate the creation of mandates, payment submissions, failure handling, and customer communications.

GoCardless provides pre-built integrations with numerous platforms for users who do not want to start from scratch. These include CRMs like Salesforce, e-commerce platforms like Zuora and Magento, accounting software like Xero and QuickBooks, and billing systems like Chargebee and Recurly. The time and complexity required to start accepting payments are decreased by these integrations.

Moreover, Zapier support makes it easy to connect GoCardless with hundreds of third-party applications without coding. This accessibility opens the platform to businesses that may not have developer resources but still want automation. While the API is powerful, it’s also an area where businesses must invest some time during the setup phase. Smaller businesses without a tech team may find more plug-and-play options in other services, but the flexibility GoCardless offers is notable for scaling and customizing workflows.

User Interface and Dashboard Experience

GoCardless offers a web-based dashboard that is clean, modern, and functional. The interface is designed to serve users across departments, from finance teams to customer support. It gives users access to all critical data in a logical and intuitive layout, with minimal clutter.

From the main dashboard, users can view recent payments, track mandates, and monitor failed transactions. There’s a clear visual breakdown of which payments are pending, paid, or failed, helping businesses stay on top of cash flow. Additionally, customer records can be searched and edited easily, with all payment history stored in one place.

Setting up new customers is straightforward, typically requiring just an email address and name to initiate the mandate process. Once authorized, the system takes care of collecting payments on schedule, and users are notified of any issues.

Another appreciated feature is the exportable reports. Users can generate reports on payment performance, mandate statuses, and bank responses, which can be useful for reconciling accounts or identifying patterns in failed payments. For more advanced needs, data can be accessed through the API for custom reporting.

The interface is responsive and works well across devices, but mobile-specific functionality is somewhat limited compared to full desktop use. Still, for day-to-day tasks like monitoring or approving payments, it’s more than sufficient. Overall, the dashboard strikes a balance between simplicity and depth, making it approachable for non-technical users while still offering advanced functionality when needed.

Pricing and Fee Transparency

GoCardless uses a transparent pricing model that is based on transaction volume. For most domestic transactions in supported countries, the standard fee is 1% of the transaction amount, capped at a certain limit (for example, £2 in the UK). International transactions and those involving currency conversion typically incur additional fees.

The absence of setup fees, monthly fees, or other hidden expenses is one benefit of GoCardless’ pricing. Because of this, it appeals to startups and small enterprises seeking predictable costs. The pricing scales reasonably with volume and is easy to understand.

There are some trade-offs to take into account, though. Generally speaking, settlement times are longer than those of card processors. For instance, it may take three to five business days in the United Kingdom for a payment to be fully credited to the merchant’s account. Businesses that depend on faster cash flow may find this delay to be a drawback, even though it is normal for Direct Debit systems.

There are also additional costs for features like Instant Bank Pay, which are calculated differently and may not follow the standard capped fee model. For businesses with complex needs or higher volumes, GoCardless offers custom pricing plans that include volume discounts and premium support. In general, the pricing model is competitive, especially for recurring billing scenarios where card fees can add up quickly. But businesses should evaluate their cash flow needs and payment timings before committing to a Direct Debit-centric model.

Security, Compliance, and Reliability

Security is a critical component of any payment system, and GoCardless takes this responsibility seriously. The company is authorized by the Financial Conduct Authority in the UK and complies with relevant financial regulations in each of the countries where it operates. It is also ISO 27001 certified, which reflects its adherence to international information security standards.

GoCardless uses bank-grade encryption protocols to protect data during transmission and storage. Customer information is never shared unnecessarily and is securely stored in compliance with GDPR and other regional data protection regulations. Additionally, GoCardless operates on a secure, redundant infrastructure with high uptime to ensure business continuity.

When it comes to payment reliability, the platform performs well. Direct Debit as a method is inherently more resistant to chargebacks than card payments, and payment errors are relatively low due to built-in validation checks. In the case of disputes, the customer protection mechanisms tied to Direct Debit schemes ensure that users can reclaim funds in genuine cases of unauthorized debits.

However, merchants need to be aware that Direct Debit does come with some risks, such as delayed settlement or the possibility of funds being clawed back in the case of customer disputes. GoCardless provides tools and notifications to help businesses manage this risk effectively. In terms of overall reliability, GoCardless ranks high for platform stability, regulatory compliance, and data protection, making it a trustworthy option for businesses handling recurring payments.

Global Reach and Multi-Currency Support

GoCardless has steadily expanded its international footprint over the past few years. Currently, it supports payment collection in over 30 countries, including the UK, US, Eurozone, Australia, New Zealand, Sweden, Denmark, and Canada. This wide coverage makes it attractive to businesses with customers spread across multiple geographies.

GoCardless offers multi-currency support through its FX capabilities. Although there may be foreign exchange fees, businesses are able to receive funds and collect payments in the local currency of their customers. Customers benefit from a more localised payment experience and less hassle with international billing. The platform’s unified dashboard and API, which let users handle all international transactions in one location, is another plus. GoCardless manages the backend through its international banking network, so businesses don’t need to open bank accounts in every nation to function.

The system still depends on the local Direct Debit version in each nation, so service availability may differ slightly between areas. For instance, ACH in the US and SEPA in Europe have different requirements and processing schedules.

Despite some variability, the platform’s global capabilities are a key differentiator for businesses that want to expand internationally without building separate systems. That said, it is more focused on developed markets and may not support all regions where card-based systems are already deeply entrenched.

Customer Support and Onboarding Experience

GoCardless offers a structured onboarding process that includes access to setup guides, videos, and help articles. New users can sign up online and start accepting payments fairly quickly, often within a few days. The platform guides merchants through mandate creation, customer setup, and integration, which helps reduce the technical learning curve.

Customer support is available via email, help desk, and live chat, although phone support is typically reserved for users on advanced plans. The help center is well-organized, covering a wide range of topics from API errors to currency support. For businesses integrating through third-party platforms like Xero or Salesforce, there are dedicated help articles to simplify the process.

Feedback on support responsiveness is generally positive, especially for users on higher-tier plans. However, some small businesses on standard plans have noted slower turnaround times during high-demand periods. It’s also worth noting that GoCardless does not provide 24/7 support, which may be a limitation for global businesses operating in different time zones.

For enterprise users, GoCardless offers account managers and tailored onboarding assistance. This can be helpful for larger-scale integrations or businesses transitioning from legacy billing systems. Overall, the onboarding experience is smooth, and support is reliable, although smaller users may occasionally experience delays in response times.

Best Use Cases and Business Fit

GoCardless is best suited for businesses that depend on recurring payments or invoice-based billing. This includes industries like SaaS, fitness memberships, insurance, accounting, and education. Its strength lies in automating collections and reducing administrative overhead associated with manual invoicing and follow-ups.

Businesses that wish to reduce transaction costs and are at ease with slightly delayed settlements will find the platform particularly useful. Additionally, it’s a good option for B2B companies with customers who would rather pay with bank transfers than credit cards. GoCardless is less suitable, though, for use cases like e-commerce or point-of-sale transactions that call for real-time payment authorisation. Additionally, it lacks native support for card payments, which may be a deal-breaker for companies that wish to provide both bank-based and card-based payment options.

Additionally, the platform is not a good fit for high-risk industries or those with frequent chargebacks, as Direct Debit mechanisms have different protection rules compared to card schemes. Businesses with one-time, high-ticket transactions might also prefer faster-settling options. In short, GoCardless is not trying to be a universal payment processor but rather a focused solution for predictable, repeatable payments. When used in the right context, it can provide cost savings, operational efficiency, and a smoother experience for both businesses and customers.

Pros and Cons Summary

GoCardless offers a clear value proposition to businesses focused on recurring payments. Its biggest strengths lie in simplicity, affordability, and automation. The absence of card networks reduces fees and payment failure rates, and the API offers deep customization for businesses that need it. Multi-currency support and integrations with popular business tools enhance its usability for global teams.

Yet, there are restrictions. Cash flow may be impacted by settlements taking longer than card processors. Since Direct Debit is used so often, it isn’t the best option for all customers; some might be reluctant to share their bank information or would rather pay with a credit or debit card. Additionally, despite recent initiatives through Instant Bank Pay, there is limited support for one-time payments.

Although the platform excels in particular use cases, it is not intended to take the place of full-suite processors such as PayPal or Stripe. GoCardless is a very useful tool for companies that use recurring billing or who want to simplify their Direct Debit collection process. It is ultimately a specialised platform that fulfils its primary promise, but it needs careful consideration to make sure it aligns with a company’s payment strategy.

FAQs

Q1: Can GoCardless be used for one-time payments or only recurring billing?

While GoCardless is primarily built for recurring payments, it does support one-off transactions through features like Instant Bank Pay. However, its main value still lies in ongoing billing relationships.

Q2: How does GoCardless compare to Stripe or PayPal for small businesses?

GoCardless is more cost-effective for recurring bank payments but lacks card support. Stripe and PayPal offer broader versatility but often come with higher fees for recurring billing.

Q3: Does GoCardless support instant payouts or same-day settlements?

No, GoCardless relies on traditional bank processing times. Settlements usually take 3–5 business days, though this may vary by country and payment scheme.